Help & Support

Trading Our Products - Share Borrowing

-

SGX Implementation of Requirements on Marking of Short Sell Orders

From 12 March 2013, to enhance the transparency of market activities, SGX will publish daily reports on the total value and volume of short sales for each counter. Accordingly, from 11 March 2013, SGX will require that all sell orders on their securities markets be marked.

This means that you must indicate – based on what you know about your position – whether your sell order is a short sell or normal sell order. The sell order will not be accepted if you do not indicate this to your broker or on the iOCBC trading platform. If you realise that you incorrectly indicated a sell order and it has been executed, you must – before 2pm on the next working day – ask your broker to correct the order.

It is your responsibility to ensure that the sell order is accurately indicated. Under Section 330(1) of the Securities and Futures Act, it is an offence to deliberately make an incorrect indication as this may be construed as an attempt to manipulate the market or as intentional false reporting to SGX.

Please visit SGX for more information, including how to indicate sell orders and modify wrongly indicated orders.

-

Short selling and related penalty fees

For SGX trading, you can sell shares through iOCBC provided that they are held as ‘free balance’ in your CDP Securities Account. If you are unsure of your shares balances, you may visit CDP personally to request for a copy of your latest Statement of Shareholdings or login to CDP Internet Access. Please call CDP at (65) 6535 7511 or visit www.investors.sgx.com for more information.

For Bursa Malaysia or foreign markets, you will need to ensure that your shares are deposited in OCBC Securities Nominees account. Otherwise, please ensure that transfer of the foreign shares is arranged to facilitate your sales of shares through OCBC Securities.

To avoid any failed trades, investors are strongly encouraged to buy and sell through the same brokerage company and under the same trading account number. An investor who buys shares through a broker at Company A and immediately sells the shares through another broker at Company B must make advance payment to Company A on Trade date before 8pm via EPS or bill payment so that the shares can be settled in time for delivery on T + 2 market day (before 1.30pm).

If you have sold the wrong shares or wrong quantity, kindly perform a buyback on your own immediately on the same trading day. You will not be able to perform a buy back on your own on the subsequent day to cover this short-sold position as the due date of the purchase contract will be after that of the short-sold position.SGX will regard the sale transaction as a short-sell and will conduct a buying-in on due date if:

- You are unable to cover back the short position on the same trading day ; or

- You do not have sufficient “free balance” securities in your CDP account by 1.30pm on due date (i.e. T+2 market days) for delivery*.

* Note: With effective settlement date of 14 December 2009 onwards, CDP will not accommodate any withdrawal of buying-in requests on T+2 should the securities subsequently become available on T+2 after the 1.30pm cut-off time.

Penalty fees for buying-in by SGX

Buying-in is completed by SGX at the end of trade date + 2, settlement date will be on the next busness day. In the event buying-in by SGX is unsuccessful on trade date + 2, SGX will continue on trade date + 3. SGX will impose a penalty of S$1000 or 5% of the value of the failed trade for all buying-in (whichever is higher). OCBC Securities reserves the right to cover such fine / penalty arising from the failed delivery from the client.

Other fees for buying-in

Processing fee by SGX: S$75 per contract

Commission charged by SGX: 0.75% of contract value

Note:

All fees are subject to the prevailing GST rate.

You will need to settle any losses and fees that were incurred from the buying-in conducted by SGX.

Buy-in Price by Exchange

For SGX, the buy-in price will be minimum 2-bids based on previous day closing price, current last transacted or current bid price whichever is higher.

For Bursa Malaysia, the buy-in price will be 10-bids above the prevailing market price.FAQ

Frequently Asked Questions

(1) What is the process of borrowing shares?

Assumptions:Security Name LDP(S$) PCF(%) (1) (2) GL 0.8 90% GLP 2.77 100% Capitaland 3.24 100% SBL interest rates and charges

The borrowing fee charges yearly are 10% of the market value of the borrowed stock i.e. about 0.192% weekly (the market value will be marked daily based on the previous closing price). The fees are subject to GST.

Example:

Let’s assume that the market value of the borrowed stock is constant throughout the borrowing period. Hence, the borrowing fees of a $10,000 stock for 7 days (10% X 10,000 x 7/365) is about S$19.18 (excluding GST).

The fees will be deducted monthly from the cash balances in your Share Borrowing Account and you will receive monthly statements.

You will be charged interest on any negative balances which could result from:

i. Monthly share borrowing fees debited

ii. Buy-back of the borrowed shares at a higher price

iii. Forced buy-back by the company

iv. Any other circumstances that results in a negative balance

The negative balance will be charged at an interest rate of 2 % above OCBC Prime rate.

You are required to settle all negative balances immediately upon receipt of the monthly statements.A list of CDP charges, handling charges and other charges is appended below for your information.

Charges Amount Deposit of securities as collateral into OCBC Securities S$10* per counter (charges levied by CDP) currently absorbed by OCBC Securities Pte Ltd Withdrawal of securities as collateral from OCBC Securities into your CDP account S$10* per counter (charges levied by CDP) Rights application fee Handling fee: S$10*

Cashier's orders: S$5Dividend collection fee 1%on net dividend

Minimum:S$5 / US$5*

Maximum: S$200 / US$200*All taxes, duties and levies (including without limitation, GST) imposed by Singapore law Stipulated by Singapore law

*All fees are subject to GST. Charges are subject to change without prior notice.Education Article 1: The Fallacy of Shorting

Can you name one taboo subject that comes to your mind about stocks trading? Well, often enough for many, it is short selling.

Have you ever wondered why “short selling” was causing so much commotion during the crises?

When we talk about short selling, it is important that we discern the difference between naked short selling and covered short selling. Naked short selling refers to selling shares that are not in possession without first borrowing the shares and subsequently failing to deliver on settlement day. On the other hand, covered short selling refers to the selling of borrowed shares. Another point to note when evaluating the “impact” of short selling is the context and market structure in which one is trading.

It is often believed that short selling is detrimental to the capital markets. In 2008, the SEC in the United States banned “abusive naked short selling”. Just how much do we know about short selling in the United States and how is it different from that in the Singapore market before generalizing that short selling is “evil”?

Differences between US and Singapore markets in Short Selling

When short selling was banned in the United States, it was mainly the banning of naked short selling. Naked short selling in the United States is not necessary illegal if the broker-dealers have grounds to believe that the sale securities can be delivered. If the seller fails to deliver the sold securities on settlement day, it will be labeled as “failure to deliver”. Given a limited period, the transaction can remain unsettled until short seller closes out the position (buy-back) or borrows the shares to deliver. The sales will be sitting opened and in this case, the buyer will not be receiving the shares and seller will not be receiving the sales proceeds.

By allowing the short to sit open, it is actually creating phantom shares in the market, which has been argued that this dilutes the company’s shares. This could be a reason that share prices are artificially depressed for as long as the short is unsettled. “Abusive naked short selling” is arguably “evil”. The SEC hence enacted Regulation SHO in January 2005 to address this issue by requiring broker-dealers to close out the “failure to deliver” position after 13 consecutive days.

On the contrary, short selling in Singapore market is a totally different game.

Besides compulsory buying-in on settlement day on “failure to deliver” transactions by the Singapore Exchange to avoid creating “phantom shares”, it has to be noted that naked short selling is forbidden in Singapore. The Singapore Exchange penalizes the naked short sellers through various means of enforcements. Hence, covered short selling here is not necessary “evil” for the market because it leads to efficient capital allocation in the capital market facing an unsustainable upward trend. It also helps buyers who want to go long on the company’s securities but want to be limited in their risk exposure to buy at lower prices.

Is short selling necessarily the cause of the declining value of a quality stock?

Not really, because if the company is fundamentally strong, the efficient market hypothesis tells us that the stock is less likely to lose its value in the long run. The case of the declining value of a stock price is likely due to the substandard quality of the stock that loses its investors’ willingness to acquire the stock for more than its worth after a price correction.

There is a saying “The market takes the stairs up and the elevator down”, as an investor, do you prefer to only participate in the trek up the stairs or would you also like to capitalize on the elevator down. If your answer is the latter, there are various ways for you to do so. In OCBC Securities, you can enter into a covered short selling transaction by borrowing shares.

Call your Trading Representative now to know how to borrow shares and be prepared for the downward trending market.Education Article 2: The Tool for Shorting

The existence of the capital markets is to allocate capital efficiently. No one will be betting on the continuation of an un-sustainable upward trend. There is always a saying “What goes up must come down”. Covered short selling is not necessary bad because it helps to send price signals and correcting / reallocating resources to improve the efficiency in the capital market and thus bringing the supply and demand of the company’s stocks to equilibrium.

Covered short selling is the act of borrowing the respective stocks first before engaging into a “selling without possession” activity. So, what is borrowing of stocks all about?

Securities borrowing (and lending) or also known as SBL has come a long way. Popularized since the 1970s, it is now a long-established practice and has become an integral part of today’s capital markets. SBL is a temporary loan of securities by a lender to a borrower where in return, the lender receives a fee. The lender may at anytime recall the securities and the borrower is obliged to return the securities on demand or at the end of any agreed term.

The word “lending” can be misleading in some ways because in law, securities lending transaction is in fact an absolute transfer of title against an undertaking to return equivalent securities. Therefore, the lender no longer owns the securities and the economic benefits of owning the securities such as dividends. To guard the interest of the lender as a shareholder, the borrower is obliged to make (“manufacture”) equivalent payments back to lenders for the economic benefits which the lender is entitled to. Also, the lender is given the contractual right to recall the securities from the borrower at any time. In addition, the borrower will have to collateralize the transaction with cash or equivalent to protect the lender against counterparty credit risk.

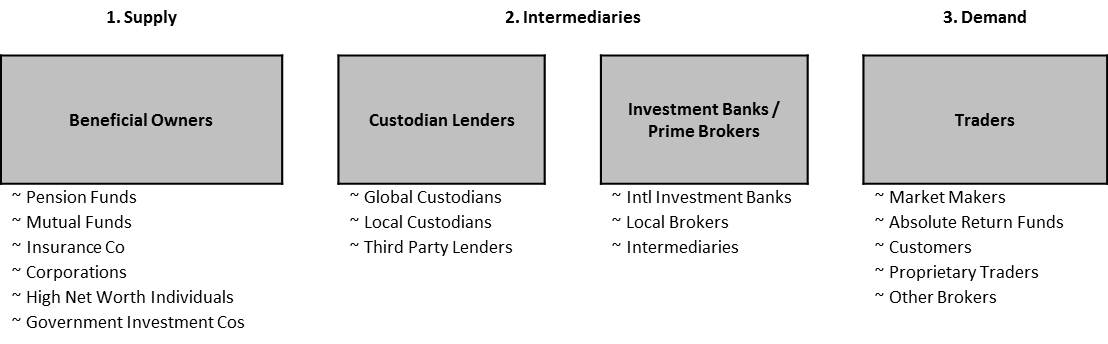

On the supply side of the equation, the market participants of securities lending consists of beneficial owners who are mainly the owners of pension funds, mutual funds, insurers, corporations, high net worth and government investment companies. On the demand side, one will see market makers, hedge funds, individual traders, brokers, proprietary traders.

Education Article 3: The Mechanics of Shorting in OCBC Securities

Short selling (covered) in OCBC Securities can be as easy as 1-2- 3.

With the borrowed securities, you can now sell first without owning the shares and buy back at a later time yet not having to fear the mandatory buying-in by the Singapore Exchange.

Step 1: Check Availability for Respective Stocks via your Trading Representatives

Step 2: Deposit in sufficient collateral into your SBL account

How much collateral is sufficient? In OCBC Securities, you can borrow up to two (2) times the value of your collateral provided. Collateral is accepted in the form of cash or securities.

Step 3: Flag and short sell in cash market

After you have bought back the shares using your SBL account, you can choose to return or hold on to the borrowed securities for future uses.

Why OCBC Securities?

- SBL account is FREE

- ZERO admin fee

- ZERO account maintenance fee

- Minimum loan is ONLY 3 market days

Standby your SBL account for the right moment for short selling

Call your Trading Representative now to find out more about OCBC Securities’ SBL services.